The following page is intended to provide you with the latest updates and news as it relates to federal student loans. We will continue to monitor changes and provide borrowers with the latest information here.

IMPORTANT UPDATES: Federal Student Loan Debt Relief, Repayment Restart, and SAVE Repayment Plan

Student Loan Debt Relief: The Supreme Court issued a ruling prohibiting the U.S. Department of Education from implementing the Biden-Harris Student Debt Relief Plan. Official guidance and updates are available at: https://studentaid.gov/manage-loans/forgiveness-cancellation/debt-relief-info

Repayment Restart: Federal student loan interest will resume starting on September 1, 2023, and payments will be due starting in October. We have launched a Student Loan Repayment Restart Webpage to support borrowers as they prepare for and navigate repayment restart. You’ll also find more information on how to prepare for repayment restart at StudentAid.gov.

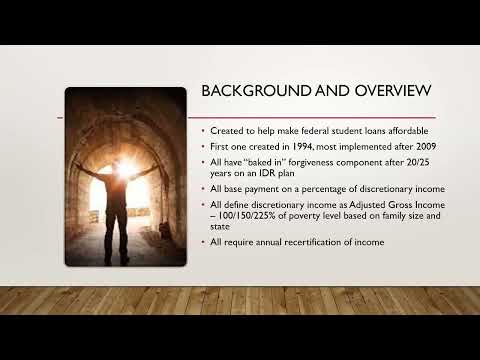

SAVE Repayment Plan: The Saving on a Valuable Education (SAVE) Plan replaces the existing Revised Pay As You Earn (REPAYE) Plan. Borrowers on the REPAYE Plan will automatically get the benefits of the new SAVE Plan and may be able to reduce their monthly loan payments. The SAVE Plan, like other income-driven repayment (IDR) plans, calculates your monthly payment amount based on your income and family size. The SAVE Plan provides the lowest monthly payments of any IDR plan available to nearly all student borrowers. Learn more at StudentAid.gov.

Income-Driven Repayment Account Adjustment for Eligible Borrowers

The Department of Education will conduct a one-time adjustment of IDR-qualifying payments for all William D. Ford Federal Direct Loan (Direct Loan) Program and federally owned Federal Family Education Loan (FFEL) Program loans. This one-time account adjustment will apply to borrowers who are:

- on an income-driven repayment (IDR) plan or were on one in the past;

- in the Public Service Loan Forgiveness (PSLF) program; or

- not on an IDR plan but are interested and have Direct or Federal Family Education Loan (FFEL) Program loans held by the U.S. Department of Education (ED).

The adjustment will be applied to most borrowers’ accounts in 2024. It will be applied only to Direct and FFEL Program loans held by ED.

If you have commercially held FFEL or any Perkins or HEAL loans, you will need to consolidate before the end of 2023 to benefit from the account adjustment.

For more information, including an FAQ, please visit the Department of Education’s Payment Count Adjustments Toward Income-Driven Repayment and Public Service Loan Forgiveness Programs webpage.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness Program (PSLF) is a program that forgives the remaining balance on Federal Direct Loans after a borrower has made 120 qualifying monthly payments while working full-time for a qualifying public service employer.

To qualify for PSLF, you must:

- Be employed by a U.S. federal, state, local, or tribal government or not-for-profit organization (federal service includes U.S. military service);

- Work full-time for that agency or organization;

- Have Federal Direct Loans (or consolidate other federal student loans into a Federal Direct Consolidation Loan);

- Repay your loans under an income-driven repayment plan; and

- Make 120 qualifying payments.

PSLF Resources

- Public Service Loan Forgiveness (PSLF) Help Tool

- Public Service Loan Forgiveness (PSLF) & Temporary Expanded PSLF (TEPSLF) Certification & Application

- Limited PSLF Waiver Information

- Public Service Loan Forgiveness Program FAQ

Presentations

Federal Student Loan Updates

November 3, 2023 — This month’s Financial Check-In with FAME focuses on what you need to know if you have federal student loans in repayment. National student loan expert, Betsy Mayotte, shares critical information and helpful tips to assist you with the One-Time Income Driven Repayment (IDR) Account Adjustment being conducted by the Department of Education. You’ll also learn about the latest news and updates impacting federal student loans.

Student Loan Repayment and Understanding the Income Driven Adjustment

August 4, 2023 — Federal student loan payments that were suspended as part of COVID relief will go back into repayment in October 2023. During this webinar, national student loan expert, Betsy Mayotte, shares critical information and helpful tips to help you successfully navigate repayment. This session includes an overview of the One-Time Income Driven Repayment (IDR) Account Adjustment being conducted by the Department of Education.

Debt Relief, PSLF, and IDR Waivers and New Information for Parent PLUS Loan Borrowers

January 25, 2023 — Offered by FAME in partnership with the State of Maine Treasurer’s Office, this presentation provides important and developing information about student loans. Nationally recognized student loan expert, Betsy Mayotte, explains what to expect regarding the Biden/Harris debt relief program, when the student loan payment pause will end, how student loan borrowers can still take advantage of the temporary exceptions available to those pursuing Public Service Loan Forgiveness, and BIG changes that impact federal Parent PLUS Loan borrowers.